Buying a condo or house-and-lot is exciting, but if financial hardships or fallouts with a co-buyer come, it can turn into a nightmare.

If this happens, many buyers on installment plans think they can no longer recover the money they paid, especially when the developer ignores them or their co-buyer makes things difficult. Many just stop paying and walk away, not realizing they may still be eligible for a refund.

As a real estate lawyer (and an accredited real estate professional), I help clients successfully cancel a condo, deal with co-buyers whom they no longer want to talk to, and maximize their recoverable money.

In 1972, Senator Ernesto Maceda enacted a law to protect people like you from onerous or oppressive conditions.

This law was called Republic Act No. 6552, or the Realty Installment Buyer Protection Law. From then on, the law was named after him, the “Maceda Law.” It delineates the rights and remedies of buyers and protects them from “one-sided and pernicious contract stipulations.”

He especially wanted to financially protect buyers on installment plans who chose to cancel their contract to sell for various reasons, including financial hardship.

So what are your rights under this law?

Rights of Buyers under the Maceda Law

Coverage and Exclusions

If your transaction involves the sale or financing of real estate on installment payments, including residential condominium apartments and houses, you are covered. In common terms, this is often referred to as “in-house” financing. The Supreme Court has held that this does not include those under bank financing (e.g., the bank paid the seller, you have paid the bank for more than 24 months, and now you seek a refund).

If the property you bought in installments is an industrial lot, commercial building, or DAR-covered land, you are not covered. If you bought in under in straight terms (usually evidenced by a Deed of Absolute Sale), you are not covered.

Maceda Law doesn’t just cover those who bought from juridical entities or corporate developers (e.g. SMDC, Megaworld, Ayala), but also individual sellers. If you bought a condo/land/house from an individual under installments, they cannot outrightly cancel your CTS and oust/eject you without complying to the procedural requisites laid down under the Maceda Law.

Rights if AT LEAST 2 years of installments are paid

- Grace Period: The buyer earns one (1) month of grace period for every one (1) year of installment payments made, to pay without additional interest. This right can be exercised only once every five (5) years.

- Cash Surrender Value (Refund): If the contract is cancelled, the seller must refund 50% of the total payments made. After 5 years of installments, an additional 5% is added every year, up to a maximum of 90%. Down payments, deposits, and options are included in this computation.

- Mandatory Cancellation Steps: Actual cancellation only takes effect 30 days after the buyer receives a notarized notice of cancellation or demand for rescission, AND upon full payment of the cash surrender value.

| It’s important to lay out the legal basis for your refund/CSV entitlement in your notarized Formal Notice of Cancellation of Contract to Sell (FNCCTS) to save you time from the developer’s denials and rebuttals. You can hire a real estate lawyer to draft this FNCCTS for you. For accuracy, send your CTS (Contract to Sell), SOA (Statement of Account), and Reservation Agreement. |

Rights if LESS THAN 2 years of installments are paid

- Grace Period: The seller must give a grace period of not less than 60 days from the date the installment became due.

- Mandatory Cancellation Steps: If the buyer fails to pay within the grace period, the seller may cancel the contract 30 days after the buyer receives a notarized notice of cancellation.

| Never take no for an answer. If you try to cancel and ask for a refund, chances are, some developers, with the goal of protecting their cash flow, may give you various reasons to avoid refunding you. In this case, a demand letter/FNCCTS with sound legal and factual foundation is valuable as it shifts the legal case to the developer’s legal team, who knows that they could lose if the matter escalates to government regulators (e.g., DHSUD, Office of the President) |

Meaning of “Installments”

All payments (including reservation fees and monthly equity) are included in the computation of installments. It refers to the monetary value (of the 24 months) rather than merely to the time duration. So, even if you have not paid for at least 24 months, but the money you have paid, including the reservation and down payment, already covers 24 months of the “installments”, you are eligible. (Orbe vs. Filinvest Land)e

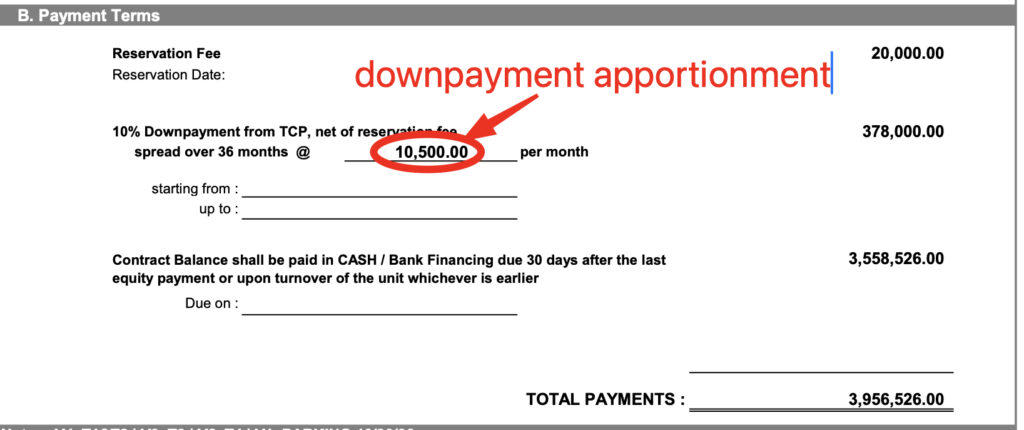

The divisor to be used must be construed in light of the purpose of Maceda Law, which is “in a manner favorable to the buyer.” (Orbe). However, the Supreme Court held that the ruling in Jestra was wrong because, in that case, the divisor used was the apportionment of the downpayment. The rationale is that “smaller, more affordable portions, x x x do not embody the ratable apportionment of the contract price throughout the entire duration of the contract term.” (Jestra vs. Pacifico) Hence, the proper divisor is not the partial installments for the down payment but the partition of the contract price into monthly amortizations.

In one developer, the formula in determining the value of the 24 months is:

TCP / 49 months = value of the 24 monthsWhy 49 months? Developers often use their standard project term, like 1 month reservation + 48 months standard equity/construction period, as a divisor, unless the buyer has already “locked-in” a specific amortization term, which is usually 5 years (common maximum term for in-house financing).

Barring any other contractual stipulations to the contrary, your entitlement to a refund depends heavily on the value of the “installments” you have made, whether or not they are equivalent to 24 months’ worth of “installments”.

Additional Buyer Rights

During the grace period and before actual cancellation, the buyer has the right to:

- Sell or assign their rights to another person through a notarial act.

- Reinstate the contract by updating the account.

- Pay the full unpaid balance in advance at any time without interest, and have this full payment annotated on the property’s certificate of title.

Effect of Invalid Cancellation

The procedures for cancellation under the Maceda Law are strictly mandatory. If the seller fails to comply, such as failing to send a notarized notice or failing to refund the cash surrender value, the cancellation is void and the contract remains valid and subsisting.

How to Cancel if you have a co-buyer

In some cases, you may have bought the condo together with your live-in partner, spouse, or friend. The relationship may have gone sour, or financial difficulties simply made monthly payments difficult.

If this is your reality, developers cannot simply cancel a contract without their explicit consent. Here are two possible scenarios:

Scenario A: Your co-buyer wants to split the proceeds with you

- The FNCCTS must be signed by all co-buyers.

- Some developers may require that the bank account be a joint account (named under both co-buyers) so that the check cannot be deposited into just one account.

Scenario B: Your co-buyer wants to waive their right to the proceeds

- One co-buyer must execute a Waiver of Rights, and it must be embedded in the FNCCTS to compel the developer to issue the refund check to only one person.

- In some cases, the waiver of rights may come with a monetary condition, such as the waiving co-buyer requiring payment. It is advisable to do this through “simultaneous swapping” (the signed document(s) are exchanged for settlement checks). To avoid any issues, please make the check a Manager’s Check.

If the co-buyers do not want to meet in person, they may authorize a lawyer (via an SPA) to represent them, execute documents, and receive correspondence/payments on their behalf in accordance with their interests.

Also, before you decide to cancel, explore the possibility of recovering 100% of your money through a “pasalo” / assumption process.

When To Escalate Matters to DHSUD

The DHSUD (Department of Human Settlements and Urban Development) is the agency of the national government responsible for managing housing, human settlements, and urban development. It replaced the previous HLURB (Housing and Land Use Regulatory Board).

- Formulating and enforcing rules over subdivisions, condominiums, and similar real estate developments.

- Environmental and land use planning and development.

- Regulating Homeowners Associations (HOAs)

You don’t start with DHSUD, but if matters get difficult with your developer, you or your authorized representative could first ask for a technical legal consultation at your local DHSUD office. However, they don’t just merely give legal advice on the spot – you want to schedule a conference meeting with the developer inside the premises of the DHSUD.

The first stage is that the DHSUD officer will try to settle the matter amicably. They will encourage the parties to talk and log the parties’ minutes and commitments. They would act as the mediator that will monitor the compliance.

If the aforesaid mediation fails, the matter may be escalated to the Human Settlements Adjudication Commission (HSAC). The HSAC is the quasi-judicial body responsible for adjudicating housing and real estate disputes in the Philippines.

If a buyer bypasses the DHSUD and files a case directly in regular courts, the complaint can be dismissed for (a) failure to exhaust administrative remedies; (b) for violating the doctrine of primary jurisdiction; or (c) lack of cause of action. However, a buyer may go directly to court only in exceptional circumstances. (Philhealth v. Urdaneta Sacred Heart Hospital 2021)

Cancel the Contract or “Pasalo”?

Maceda Law protects 50% of your money, but you could save 100% of it through the “pasalo” or assumption process. Of course, this option is not without its pros and cons.

Take note that finding another buyer is your legal right under the Maceda Law. The law provides:

Under Sections 3 and 4, the buyer shall have the right to sell his rights or assign the same to another person x x x during the grace period and before actual cancellation or the contract. The deed of sale or assignment shall be done by notarial act.

SEC. 5. of Maceda Law

Yes, you may be able to get 100% of your remitted money, but the risks include: (a) “depending” on another buyer to pay you; (b) finding another buyer may take a longer time; and (c) your or the new buyer may have to pay a “Transfer Fee.” (some developers set this at P100,000)

Finding a Buyer

The speed at which a new buyer is found also depends on the “attractiveness” of the price. If the unit was contracted by the first buyer years ago and the price has already increased dramatically, new buyers will find it attractive. Here’s an example based on an actual experience:

First Buyer (2020)

Unit Price: P2,200,000

New Buyer (2026)

Now: P3,200,000

If the “assume price” is only P2,200,000 and the new buyer will only add a P100,000 redocumentation fee now, it is better for them to get this “pasalo” unit rather than get a brand new unit for a higher price of ~1,000,000.

The “Assume” Costs

The developers would often call this “Redocumentation Fee” or “Assumption Fee,” and this costs somewhere around P50,000 to P100,000. (Quick history: Developers imposed this because many agents in the past “abused” the system by reserving a unit in their own name, and, when the price shoots up, they would sell the unit to their clients under the guise of “assumption.” To discourage this practice, hence the hefty price tag.)

Zonal Value Difference: The government views this as a sale of rights. The new buyer will have to pay Capital Gains Tax and Transfer Taxes based on the current Zonal Value, which has likely skyrocketed since the pre-selling days.

Consider the turnover date or the date the unit will be turned over to you. If you still have much time, you can find the new buyer without much pressure. If you have less time left before the turnover, you don’t want to be pressured into taking out that lump sum through a bank loan. When this date arrives, it is advisable that the new buyer already has a bank guarantee letter.

The verdict: If the current market value is high, you have a willing and able buyer or have a good broker, and the turnover date is comfortable for you and your buyer, “Pasalo” or “Assumption” is great. But if you need cash and want less “headache”, the 50% Maceda refund is the faster and safer option.

| Remember to protect your rights and your new buyer’s rights by putting everything in writing, not relying on verbal agreements or human memory. As the old adage says, “the memory of man cannot be trusted.” For a better peace of mind, work with a real estate lawyer. |

In Summary

Developers may not “run” to always remind you of how much and how you will be able to get your entitlements, as they assume that you already know the law.

Remember that you have strong and clear legal rights under the Philippine law as a buyer of residential property in installments.

It’s just a matter of how you execute and enforce your rights. Don’t leave your hard-earned money on the table.

Contact our law office for a consultation.

FAQs.

The answer depends on how long you’ve been paying. Under the Maceda Law, you are entitled to a grace period of one month for every year of installments paid. Once you stop paying the monthly installments, the developer is required to give you grace period depending on the number of years you have already paid.

Yes. The Supreme Court has ruled that all payments, including reservation fees and monthly equity, count as “installments” under the Maceda Law. But their total value must still reach the threshold of the “24 months” worth of installments.

No, not if you qualify under the Maceda Law. If a developer refuses a valid refund request, you can file a formal complaint with the DHSUD (formerly HLURB) for illegal real estate practices.

Redocumentation fees vary by developer but typically range from ₱10,000 to over ₱100,000. This may be shouldered by the first buyer or the new buyer, depending on the agreement. Additionally, the new buyer may be responsible for BIR taxes based on the updated Zonal Value of the property.